|

| Unfathomable Depths by Ibai Acevedo |

Denmark's Nationalbank and the Swiss National Bank are the world's most interesting central banks right now. As the two of them push their deposit rates to record low levels of -0.75%, they're testing the market's limit for bearing negative nominal interest rates. The ECB takes second prize as it has been maintaining a -0.2% deposit rate since September 2014.

At some point, investors will flee deposits into 0%-yielding cash. This marks the effective lower bound to rates. Has mass paper storage begun? The last time I ran through the data was in my monetary canaries post, which was inconclusive. Let's take a quick glance at the updated data.

To gauge where we are relative to the effective lower bound, I'm most interested in the demand for large denomination notes, which bear the lowest costs of storage. Once a central bank reduces its deposit rate so deep into negative territory that the carrying cost of deposits exceeds the cost of storing a nation's largest value banknote, then it has hit the effective lower bound. Small denominations notes, which have higher storage costs, are not a pivotal part of the picture given the ability of note holders to freely convert low value notes into higher ones.

European Central Bank

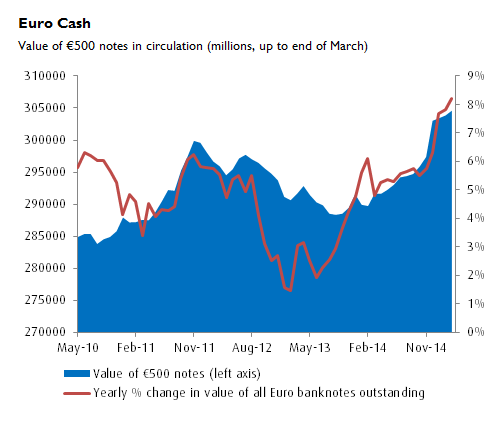

The ECB issues the €500 note, which has the second highest purchasing power out of the world's currency notes. I've charted the quantity of €500 euro notes in circulation below, as well as the percent change in the value of all euro denominations:

After declining through 2012 and 2013, we saw a sharp rise in demand for €500 notes, particularly in December 2014 and the first few months of 2015. The red line illustrates the general demand for all denominations of euro cash. Over the last four months the seasonally-adjusted growth rate of banknotes outstanding has risen to its highest level in the last five years.

It's hard to determine how much of this increase can be attributed to the ECB's negative rate policy, initiated when Mario Draghi brought the deposit facility rate to -0.1% in June and -0.2% in September, and how much is due to the Greek fiasco. Growing fears that Greece will either leave the euro or impose capital controls have led to a steady jog out Greek banks. There are two escape routes: Greek's can convert their deposits can into German deposits or into cash.

In an interesting article, Bloomberg's Lorcan Roche Kelly backs out the Greek-specific demand for European cash. Read it for the full details, but the shorter rendition is that a line item on the Bank of Greece's balance sheet allows us to see how many banknotes Greeks are demanding in excess of the Bank of Greece's regular allocation. Kelly finds a large spike beginning in December and extending into 2015, which we can attribute to the bank jog. I've recreated the chart below:

|

| Source: Bloomberg, data to end of March |

The approximately €12 billion jump in Greek cash demand corresponds nicely with the recent €7.2 billion spike in €500 notes in circulation across the entire eurozone. The upshot is that a large chunk of the rise in €500 notes over the last few months is probably due to a run on Greek banks, not an escape from negative-yielding ECB deposits. Remove the run and the rise in demand for €500 notes would have been unremarkable, indicating that the eurozone is still far from hitting the effective lower bound.

Swiss National Bank

Because Swiss banknotes are not a direct escape route from the ongoing Greek bank run, SNB cash data should provide a clearer signal of the whereabouts of the effective lower bound than ECB data. The SNB issues the world's most valuable banknote in terms of purchasing power; the 1000 franc note. Below I've plotted the yearly percent change in demand for both the 1000 note and Swiss cash-in-general to the end of February.

There's been slight pickup in the demand for Swiss cash, but nothing dramatic. Its worth pointing out that Swiss paper currency has historically played a safe haven role. Demand tends to spike during episodes of uncertainty, including the 2008 credit crisis and the 2011-12 period, when it seemed like the euro could be torn apart. This means that it is difficult to be sure how much of the recent pickup in demand for Swiss cash stems from the SNB's -0.75% deposit rate and how much is due to fear of a Greek government default, which would create havoc in world markets.

Danmarks Nationalbank

Our final canary is the Danmarks Nationalbank. Unlike the demand for Swiss paper francs, the demand for Danish paper krone does not usually spike during times of crisis. For instance, during the 2008 credit crisis demand remained muted. This leads me to believe that demand for paper krone provides the clearest indicator yet of the presence (or not) of the effective lower bound. I've charted the year-over-year change in Danish currency in circulation.

In the 55 days that have passed since the Danmarks National bank reduced its rates to -0.75% (February 5), there has been a sustained rise in the demand for cash, as the red data indicate. But I don't think we can describe it as anything out of the ordinary, at least not yet.

Interestingly, in late March the Nationalbank granted Danish banks some wiggle room by providing them with greater access to the Bank's 0% current-account facility. This small adjustment would have reduced Danish banks' incentives to emigrate from -0.75% deposits into cash. Was the central bank's decision to provide this wiggle room a response to private data showing that it had hit the effective lower bound? Who knows.

It may be worth noting even if a central bank finds itself at the effective lower bound, it can forestall the demand for large denomination notes by using moral suasion. Willem Buiter mentions this possibility in his recent note High Time To Get Low, but maintains we have no evidence of this sort of pressure. I'm tempted to agree with him. If either the Danish or Swiss central bankers have put informal embargoes on cash, we would have known about it by now.

The use of moral suasion to prevent large denomination banknote storage would effectively freeze the quantity of high value notes in circulation. In such a scenario, we'd expect the 1000 Sfr note to rise to a slight premium to face value, say 1050 Sfr in bank deposits for each 1000 Sfr in banknotes. Traders would be willing to pay this premium as long as the storage costs on high value notes are lower than the -0.75% penalty set by the SNB on deposits, thus allowing them to earn an excess return on their note holdings. As long as moral suasion remains successful in choking off Swiss banks' demand for cash, each subsequent cut by the SNB into ever deeper negative territory would drive the premium on notes higher. (Assiduous readers will recognize this as the second of three ways for a lazy central banker to escape a liquidity trap.)

In sum, we probably haven't hit the effective lower bound yet. Stay tuned.